Fertilizer Market Size and Share in Africa

Africa Fertilizer Market Analysis

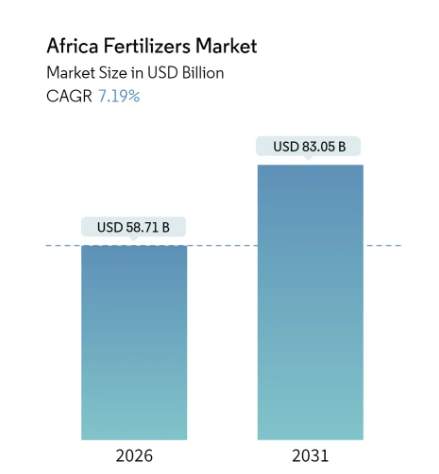

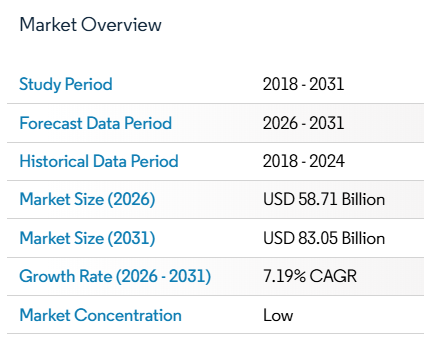

The Africa fertilizer market size was valued at USD 54.77 billion in 2025. It is projected to grow from USD 58.71 billion in 2026 to USD 83.05 billion by 2031, registering a compound annual growth rate (CAGR) of 7.19% during the forecast period (2026-2031). Steady policy coordination across the continent and the expansion of domestic production capacity support this growth, as governments prioritize input self-sufficiency and food security. Compound fertilizers dominate the market due to their balanced nutrient composition, which meets precision fertilization requirements, while new urea plants in Nigeria are boosting urea price trends. Digital agronomy, green ammonia investments, and targeted subsidies are expanding access for smallholder farmers and stimulating private capital inflows into distribution channel upgrades. Persistent logistical gaps and recurring global price spikes remain negative factors; however, sustained demand for nutrient-rich staple crop production underpins a robust growth outlook for the African fertilizer market.

Key Takeaways

By Type: Compound fertilizers accounted for 58.02% of the Africa fertilizer market share in 2025, and are expected to achieve a CAGR of 8.27% through 2031.

By Form: Conventional forms held a 90.76% share of the Africa fertilizer market in 2025, and are projected to grow at a CAGR of 7.14% through 2031.

By Application Method: Fertigation accounted for 60.93% of the Africa fertilizer market size in 2025, while foliar fertilization is expected to grow at a CAGR of 8.27% through 2031.

By Crop Type: Field crops accounted for 90.88% of the Africa fertilizer market size in 2025, and are expected to grow at a CAGR of 7.14% through 2031.

By Geography: Nigeria led the Africa fertilizer market size with a 12.37% share in 2025, while South Africa is expected to grow steadily at a CAGR of 6.41% through 2031.

Africa Fertilizer Market Trends and Insights

Driver Impact Analysis

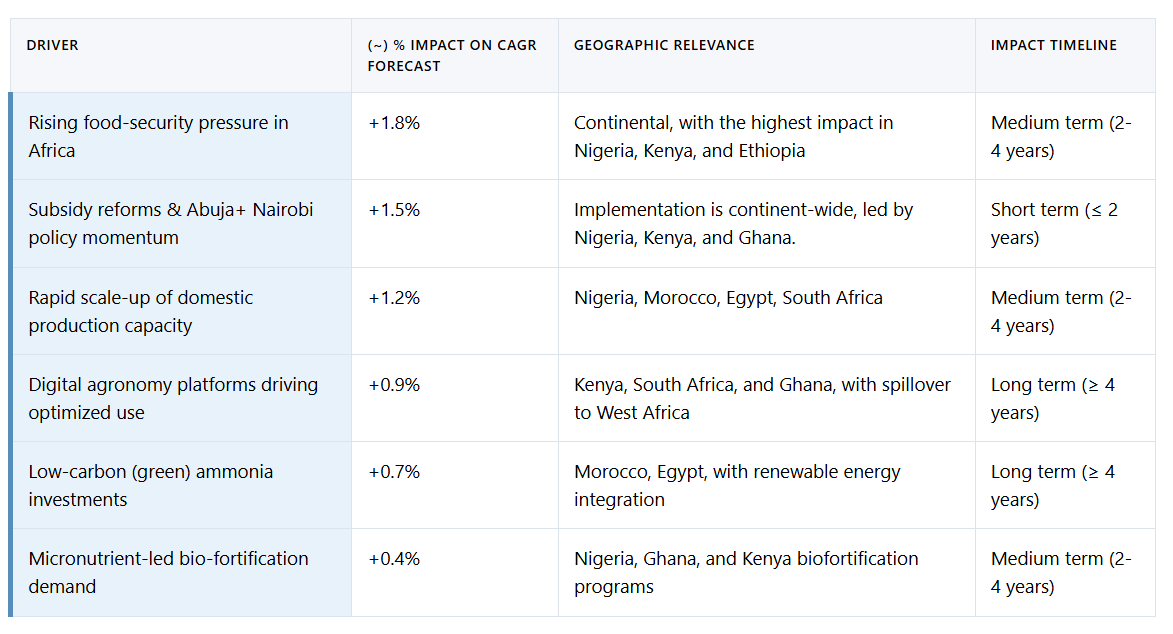

- Increasing food security pressure in Africa

- Subsidy reforms and Abuja–Nairobi policy momentum

- Rapid expansion of domestic production capacity

- Digital agronomy platforms driving optimized usage

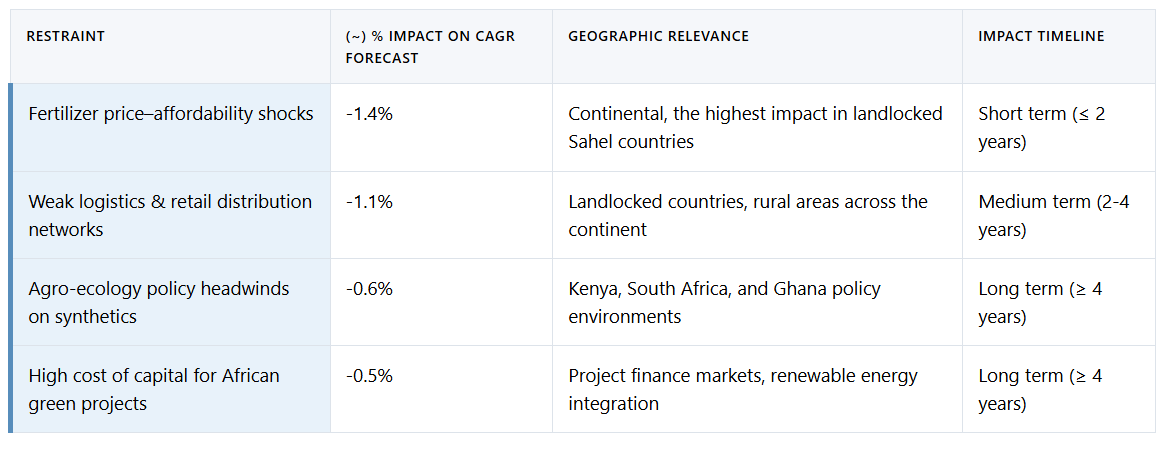

Constraint Impact Analysis

Fertilizer prices – affordability shocks

Weak logistics and retail distribution networks